An airline is a commercial company that operates aircraft to provide air transportation services for passengers, cargo, or both, typically offering scheduled flights between various destinations around the world, and it often includes a wide range of supporting operations such as ticketing, baggage handling, in-flight services, and maintenance to ensure safety, efficiency, and customer satisfaction throughout the travel experience.

The concept of ‘low-cost carriers’ or LCC originated in the United States with Southwest Airlines at the beginning of the 1970s. In Europe, the Southwest model was copied in 1991, when the Irish company Ryanair, previously a traditional carrier, transformed itself into an LCC and was followed by other LCCs in the United Kingdom (e.g. easyJet in 1995). An LCC is defined as an airline company designed to have a competitive advantage in terms of costs over an FSC. In order to achieve this advantage, an LCC relies on a simplified business model (compared with the FSC), a model which is characterized by some or all of the following key elements:

Core business: This is passenger air-service despite the ancillary offers are increasing and becoming part of the LCC core business.

Point-to-point network: The network is developed from one or a few airports, called ‘bases’, from which the carrier starts operating routes to the main destinations. Destinations are only continental within the Europian Union or the United States of America. No connections are provided at the airport bases, which function as aircraft logistics and maintenance bases.

Secondary airports: City-pairs are connected mainly from the secondary or even tertiary airports—such as London Luton—that are less expensive in terms of landing tax and handling fee and experience less congestion than the larger ones, such as London Heathrow. Small airports will strive to gain the LCC’ operation and the usual way is to reduce airport charges. Similarly, air transport activity generates welfare that is a multiple of the airports’ activities, inducing regional economic and social development. Local authorities recognize that the LCC operation is a potential driver for social and economic developments, and are willing to provide financial help (for example tax exemption, marketing support while LCCs start a new connection). The reduced airport fees can be understood as an incentive, as most of these secondary airports are public. These incentives can be quite relevant and can be deemed to contravene the European Union’s competition rules.

Single aircraft fleet: In general, the LCC operates with one type of aircraft, such as the Boeing 737 series with a configuration of 149 seats. The fleet composition also depends on the fact that they operate on only short- or medium-haul routes.

Aircraft utilization: The aircraft is in the air, on average, more hours a day compared with FSCs that have to respect the connectivity schedule.

No frills service: The product is not differentiated as they do not offer lounge services at airports, choice of seats, and in-flight service, and they do not have a frequent flyer program. Fare restrictions are removed so that the tickets are not refunded able and there is no possibility to rebook with other airlines.

Minimized sales/reservation costs: All tickets are electronic and the distribution system is implemented via the Internet or telephone sales centre (only direct channels). Passengers receive an e-mail containing their travel details and confirmation number when they purchase. The LCC does not intermediate the sale with travel agents and nor does it outsource the distribution to GDS companies.

Ancillary services: LCC increasingly have revenue sources other than ticket sales. Typical examples are commissions from hotels and car rental companies, credit card fees, (excess) luggage charges, in-flight food and beverages, advertising space. The potential growth of this revenue comes from telephone operations and gambling on board. Ryanair’s revenue from sources other than ticket sales contributed £259 million to its 2005–06 net profit of £302 million. Those revenues already represent 16 percent of the carrier’s total revenue. For easy Jet, that kind of income originally represented only 6.5 per cent of the airline’s total revenue, but it increased by 41.3% from 2004. Not every low-cost airline implements all of the points mentioned above. For example, in 2005 Air Berlin started the UK domestic services as feeders to its German services out of Stansted, exploring the hub-and-spoke operations. The differences between the FSC and LCC business models are multifaceted. The significant structural cost gap between the two models results from these fundamental differences.

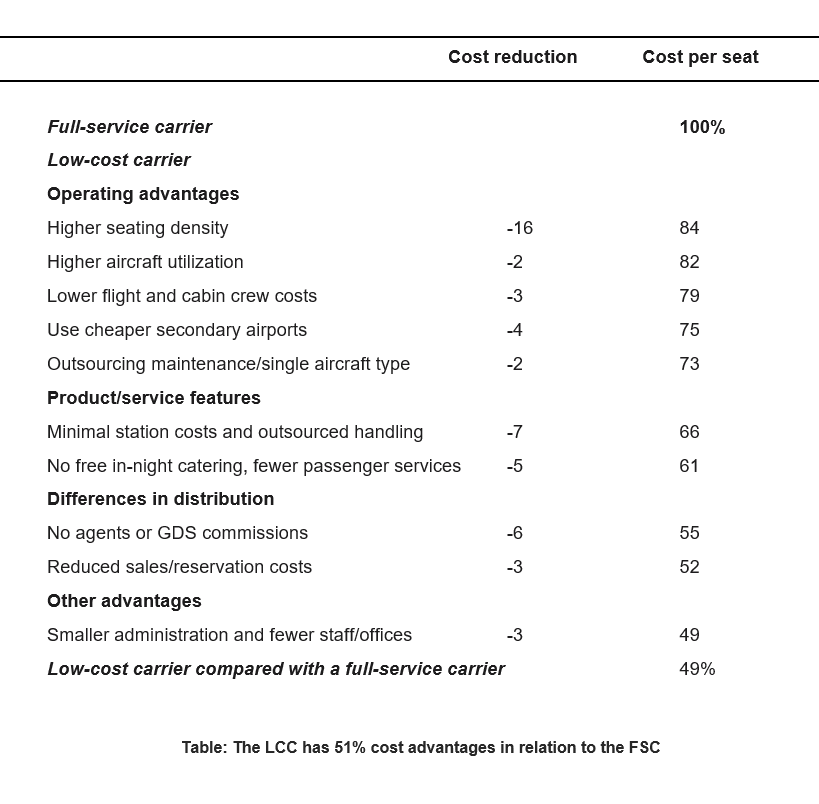

The table breaks down the cost gap between the FSC and the LCC business models. Overall, the LCC model can operate at 49% of FSC costs. In particular, 37% out of a total 51% of costs difference can be attributed to explicit network and airport choices (or business place and process complexity); another 9 per cent of the LCC cost advantage comes from the distribution system and commercial agreements (costs which are narrowing with the elimination of commissions and GDS).

A remarkably small proportion (13%) of the cost differential is product/in-flight service related. The relative simplicity or complexity of their business models distinguishes the LCCs from the FSCs. LCCs have successfully designed a focused, simple operating model around nonstop air travel to and from high-density markets.

On the other hand, the FSC model is cost-penalized by the synchronized hub operations (e.g. long aircraft turns, slack built into schedules to increase connectivity) that implicitly accept the extra time needed for passengers and baggage to make connections. In addition, the FSC business model relies upon highly sophisticated information systems and infrastructure to optimize its hubs. The most relevant success factors of LCCs are their network configuration and their streamlined production processes in relation to FSCs.

May, 20, 2026

May, 20, 2026